Chapter 4 – Understanding the Past

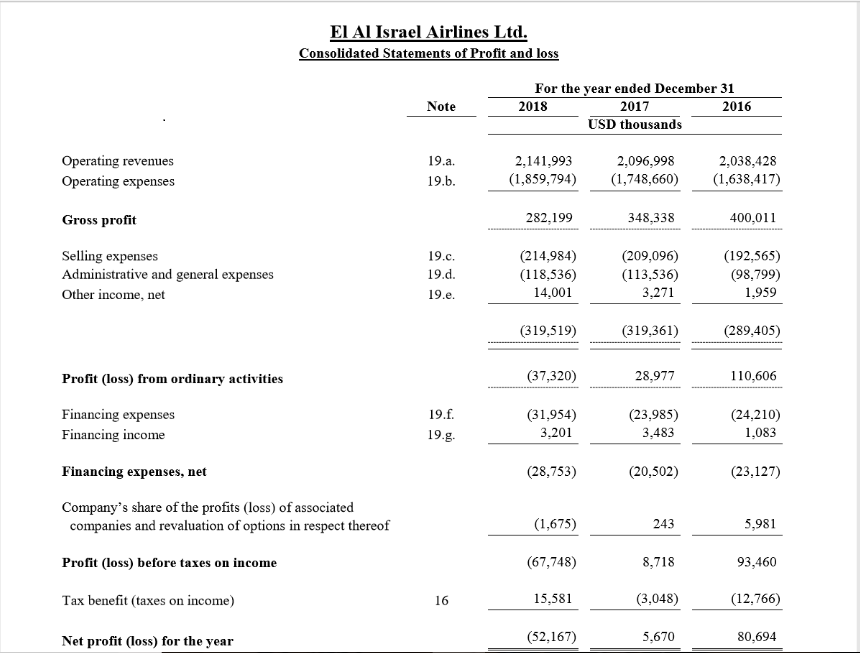

When reading about restating a firm’s financial statements, the section about clearly separating a firm’s operating and financial activities triggered something in my brain which then had me thinking about doing this in a previous unit of Martin’s. I then went and looked at my company’s most recent annual report to see what their financial statements looked like and I found that they separate their operating revenues and expenses to give a gross profit, and separate financing expenses and revenues to give net financing expenses. Are we required to go further into these accounts to see what is exactly in them? Will some people’s process of restating their company’s financial statements be much more in depth than others?

I am worried that I may not have learnt (or remembered) enough from ACCT11059 and that restating the financial statements will be just as difficult this time around. However, after looking at the examples shown in tables 4.4 and 4.5 that Martin has done on Ryman Healthcare has helped me understand it better. A key concept I took from this section was how to differentiate between financial and operating; some may be clearer than others, however. The steps to restating a company’s Balance Sheet and Income Statement has helped me to better understand the process and has now given me the confidence to start restating my own company’s financial statements, thanks Martin! I may need to go over the tax benefit section again when doing it as this is something I do not quite understand after initially reading about this.

I am still getting very confused with the different formulas and calculations; RNOA, NFO, NOA, ROE, ATO… I am struggling to keep up. I often find that when I can apply these concepts, that is when I better understand them. I believe that when I can finally apply these concepts to my company, El Al Israel Airlines, I will finally understand what the author is saying.

Profitability seems to be a key concept and as I come across this, I was worried there would be yet another idea that would leave me feeling confused as another formula was about to be thrown my way. However, once realising it was about profit margin a little bit of weight was lifted of my shoulders. The idea of profit margin is something I look at a little bit at work and it is something I quite often hear from those I work with that have been in this career for many, many years. The formula for this is rather simple in comparison to the others that have arisen so far in this unit.

This chapter has made me excited to start restating my company’s financial statements. I’m glad Martin put an explanation to the restatement process in this chapter as I was feeling very overwhelmed with the process which was why I was putting off doing it. I definitely need to make a list of all the formulas discussed so far and try to thoroughly understand them.